TL;DR:

- The light lamb market has seen a dramatic 54% increase in the indicator since October 2023, marking a significant change in producer sentiment.

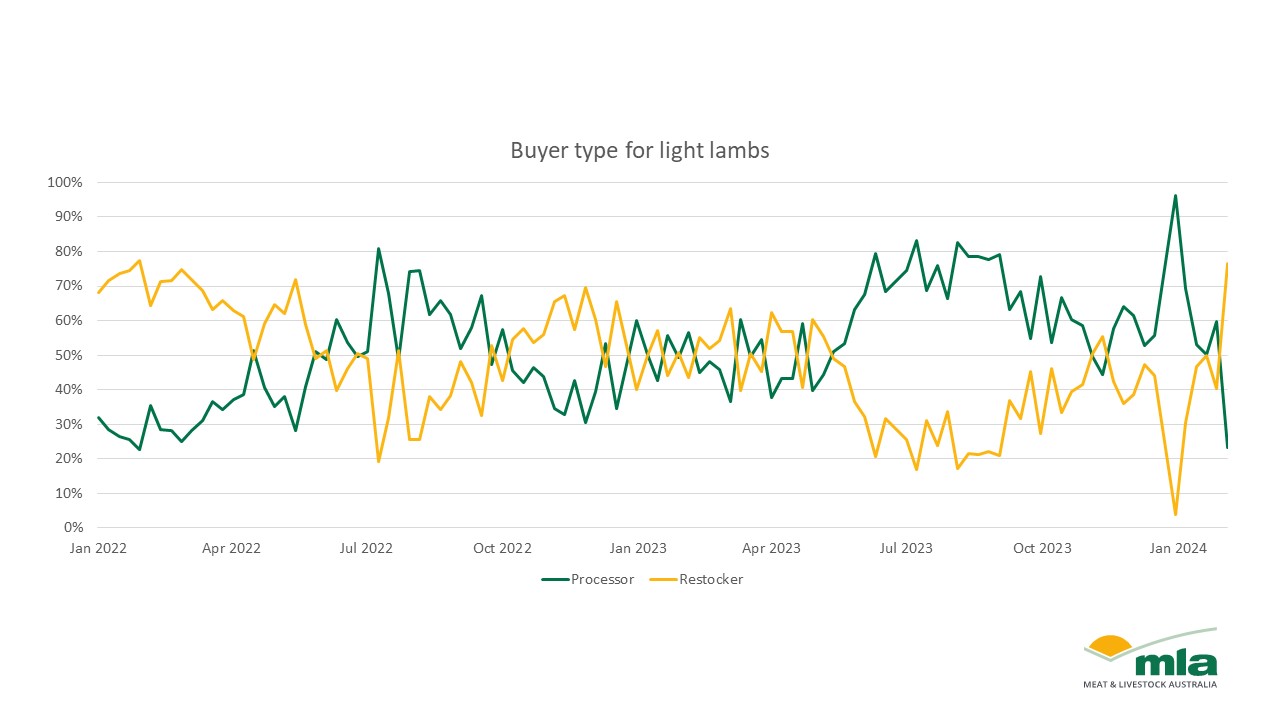

- Processors and restockers are the main buyers of light lambs, with their purchasing decisions heavily influenced by market conditions and weather forecasts.

- The majority of light lambs were sold to processors in 2023, potentially impacting the volume of lambs available in the coming autumn and winter months.

In a notable development within the lamb industry, the light lamb indicator has experienced a substantial 54% increase since October 2023. This surge reflects a marked improvement in the outlook for the year and a significant shift in producer sentiment.

Meat & Livestock Australia’s analysis reveals that processors and restockers, as the largest buyer types for light lambs, play a crucial role in shaping the market dynamics based on their purchasing decisions.

The fluctuating prices of light lambs, which have ranged from the lowest in recent memory to the highest since January 2023, underscore the volatility of the market.

The buying patterns of light lambs, driven by market sentiment and weather conditions, indicate that restockers are more likely to purchase when the market outlook is positive and weather conditions are favourable. Conversely, in less favourable market and weather conditions, processor demand for light lambs increases.

Historically, prices hovered around 800-850¢/kg carcass weight (cwt) at the start of 2022, with favourable weather conditions leading to a higher likelihood of heavier lambs being bought by restockers. This resulted in approximately 70% of light lambs being purchased by restockers, compared to about 30% by processors. However, by October 2022, the dynamic between processors and restockers became unclear, despite prices ranging from 600-800¢/kg cwt.

A significant shift occurred in May 2023, with processor demand overtaking restocker interest as prices eased from 500¢ to 300¢/kg cwt over six months, coupled with a forecasted dry season. This change in dynamics raises questions about the volume of light lambs available in 2023.

The spring flush saw 60–80% of light lambs sold to processors and 20–40% to restockers, a notable change from 2022’s distribution. With the majority of light lambs processed in 2023, the industry may face a reduced volume of lambs in the upcoming autumn and winter months, although the full impact remains to be seen.

Emily Tan, a Market Information Analyst, attributes these market dynamics to the interplay between processor and restocker demand, influenced by fluctuating prices and weather predictions. This shift underscores the evolving nature of the lamb market and highlights the need for producers to stay informed and adaptable in response to changing market conditions.