The ongoing crisis in the Red Sea is exerting significant pressure on container shipping services, directly impacting Australian red meat exporters. The conflict, primarily involving Iranian-backed Houthis from Yemen, has disrupted one of the world’s key maritime channels, leading to increased costs and extended delivery times for shipments to the Middle East and Europe.

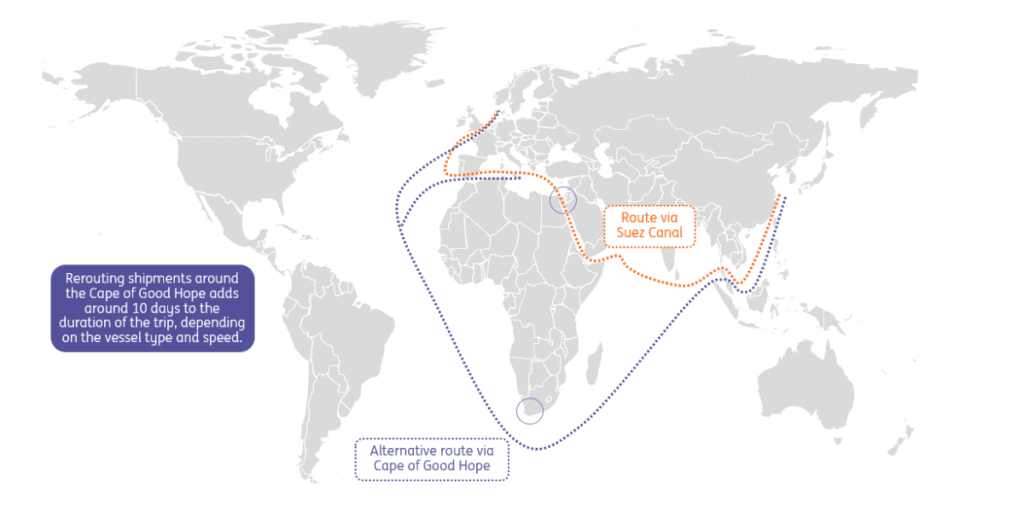

Ship owners, wary of the risks in the Red Sea and Suez Canal, are opting for the longer route via South Africa’s Cape of Good Hope. This detour adds about ten days to a typical voyage, ruling out the Panama Canal as a viable alternative due to its considerably longer distance.

Major shipping companies have responded to these challenges by increasing charges for Australian exporters. Additional fees of $500 for 20-foot containers and $1000 for 40-foot containers have been introduced. Container rates have almost tripled since the onset of the crisis in October, approaching the record highs experienced during the 2020 Global Pandemic.

The crisis has also led to prolonged delivery times and a shortage of containers. Recent attacks in the Red Sea have intensified, with no immediate resolution in sight. In December, 80% of container vessels on the Suez route were forced to alter their course, a figure that rose to 90% in early January.

The largest container freight operators, including MSC and Maersk, have diverted numerous vessels around the Cape, a trend followed by other lines like Hapag Lloyd, Cosco, ONE, and Evergreen. This shift affects 12% of global trade, including significant Australian exports and imports.

The British Chamber of Commerce noted a drastic reduction in containers passing through the Suez Canal, with rates for containers escalating rapidly. The World Bank warns that continued attacks could disrupt key shipping routes, potentially leading to inflationary bottlenecks and spikes in energy and commodity prices.

Australian agriculture is particularly vulnerable to these developments. Rabobank highlights the challenges for Australia’s agricultural sector, with canola exports to the EU being the most affected. Conversely, Australian wheat and barley might gain a competitive edge in Asian, Middle Eastern, and Eastern African markets.

Imported goods, such as fertilisers, ag chemicals, and machinery parts, are also facing higher freight costs. However, these are not expected to reach the heights of the 2021 freight crisis. The FBX global ocean freight container index has more than doubled recently, yet remains below the peak levels of 2021.

This situation presents a complex scenario for Australian trade, with potential implications for global inflation and financial markets. The Red Sea/Suez crisis, compounded by the ongoing Black Sea/Ukraine crisis, poses a risk of further inflationary supply shocks, challenging the predictions of easing price pressures and rate cuts in 2024.