After nearly three years of dwindling profitability, beef processor margins are witnessing a revival this year, primarily due to decreased livestock input costs, as reported by Beef + Lamb New Zealand.

Analyst Matt Dalgleish from Episode 3 has introduced the Beef Processor Profitability Index (BPPI), a metric based on standard processor figures.

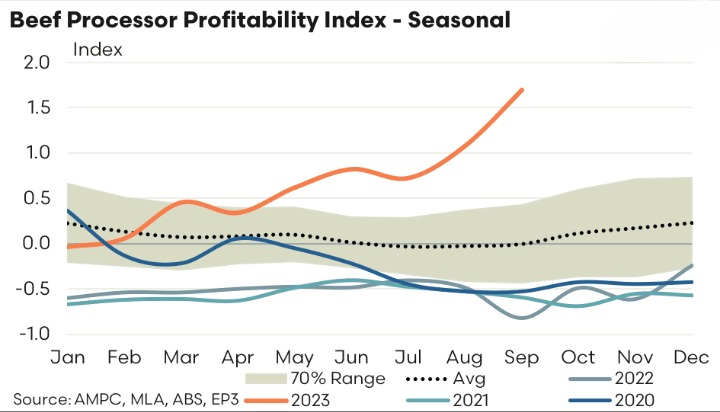

This index, first unveiled in April, was updated recently. Dalgleish commented on the sector’s transformation in 2023, noting the BPPI’s shift from negative to positive as local cattle prices have declined, thereby enhancing beef processor profitability.

The BPPI for September averaged at 1.69, marking its highest recorded value. However, this surge follows a 33-month stint in the negative. Historical data reveals that the BPPI remained predominantly negative since early 2020, plunging further in 2021 and 2022, before rebounding in 2023.

Dalgleish remarked that consistent profits haven’t been observed since the end of 2019 or the start of 2020.

Dalgleish clarified that the BPPI, a theoretical representation of the Australian beef processing sector, doesn’t imply universal profitability or loss for all processors. A negative BPPI indicates a challenging trading environment, while a positive one suggests a more favourable scenario.

Recent labour cost hikes in the red meat processing sector have also emerged. The Pacific Australia Labour Mobility (PALM) scheme, not accounted for in the current BPPI model due to data constraints, has been a contributing factor. Feedback from processors indicates that a PALM labour unit is costlier than a domestically sourced one, primarily due to accommodation expenses.

Other factors, such as limited workforce availability leading to increased overtime and the rise in the Temporary Skilled Migration Income Threshold in July 2023, have further inflated wage costs in Meatworks.

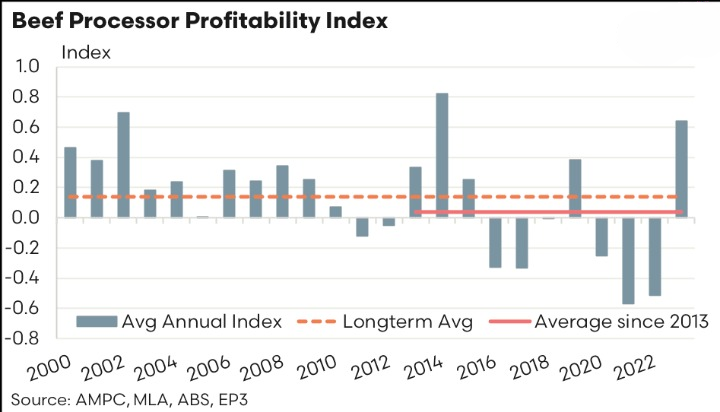

The BPPI’s trajectory in 2023 has been positive, with the third quarter witnessing a significant rise. The annual average for 2023 stands at 0.64, slightly below the 2014 peak of 0.82. The long-term average from 2000 to 2023 is 0.14. Dalgleish pointed out that the past decade has been challenging for beef processors, with a mere average BPPI of 0.04 since 2013.

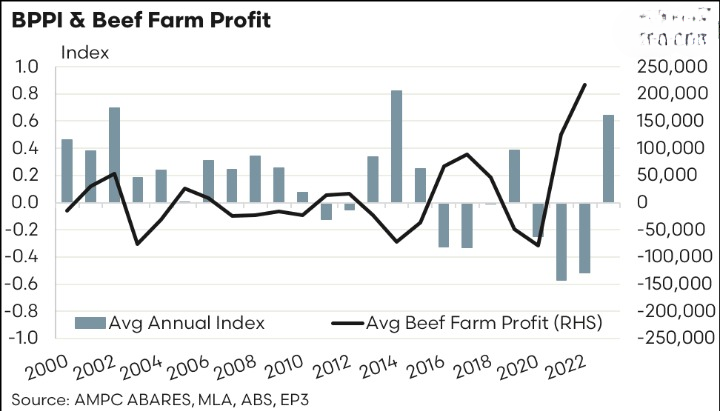

Episode 3’s data juxtaposition of annual beef farm profitability and the BPPI underscores the shift in profitability towards processors in 2023. Dalgleish anticipates a decline in beef farm profitability from its 2022 peak, given the historical trend where beef farm profitability wanes when the BPPI rises.

In the realm of direct consignment, price offers have largely remained stable this week, despite minor drops in the previous week across eastern Australia. Many processors have secured bookings until November, with some even extending to Christmas.

With the 2023 season nearing its end for several processors, some are advising farmers to make timely sale decisions, especially if they’re facing seasonal or animal welfare challenges.

In terms of slaughter numbers, the previous week saw a decline due to public holidays in NSW and Queensland, resulting in an 11% week-on-week drop to 111,125 head, the lowest since early May. Industrial action has also impacted throughput at a major Queensland plant this week.