TL;DR: Meat & Livestock Australia’s 2024 industry projections highlight a subtle decrease in the national herd size, with a shift towards more processor-ready cattle sales following a period of rebuild. Variations in cattle sales to processors and feedlots reflect both seasonal patterns and longer-term market adjustments. Queensland’s feedlot sector is absorbing more cattle, indicating a trend away from sale yard sales to direct consignment, while Victoria sees a structural shift away from dairy cattle sales.

The Australian cattle industry is experiencing nuanced shifts in saleyard throughput, reflective of broader trends in herd composition and market demand.

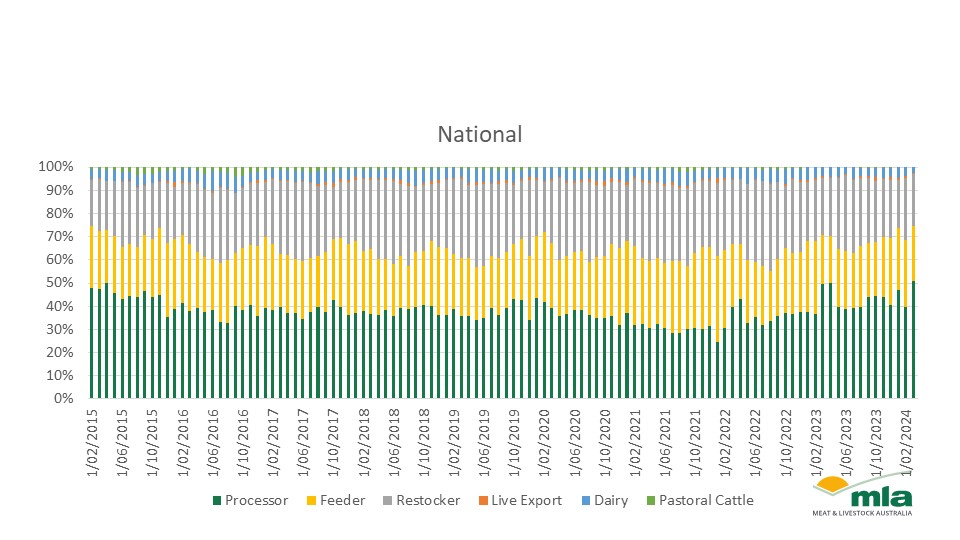

According to the latest industry projections by Meat & Livestock Australia (MLA) for 2024, the national cattle herd is expected to experience a marginal decline, stabilising at 28.6 million head by mid-2024. This follows a period of growth during the rebuild years from 2020 to 2022, wherein the younger herd has matured, leading to an increase in processor-ready animals entering the market.

During rebuild phases, the proportion of cattle sold directly to processors typically diminishes, as efforts focus on herd expansion rather than turnoff. This trend reverses as the herd matures, normalising the flow of cattle to processors.

The 2020 to 2022 rebuild saw a notable drop in processor-ready cattle sales, marking 2021 as a record-low year for such transactions across several states. This was particularly evident in New South Wales, Queensland, and Victoria, with South Australia and Western Australia experiencing delayed rebounds.

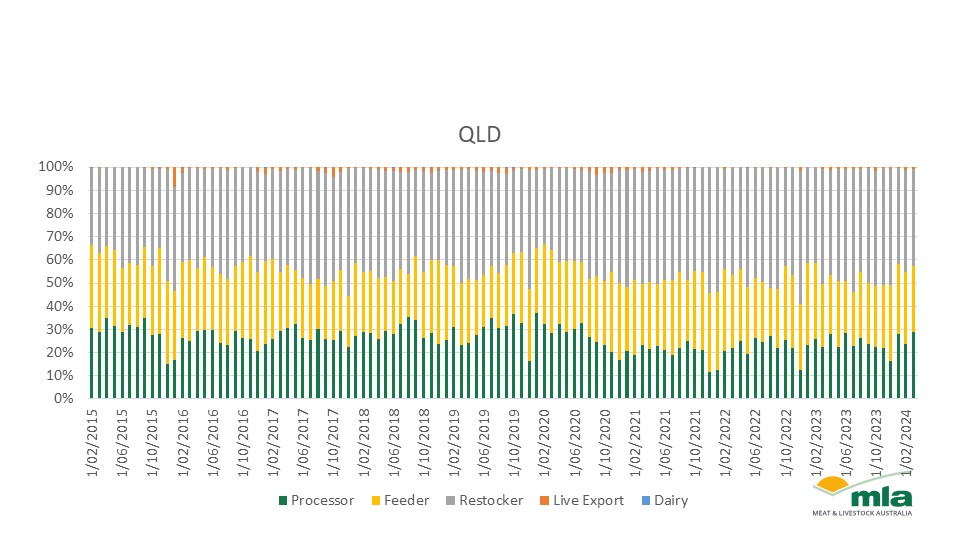

In Queensland, a significant long-term shift is observed, with a decline in processor cattle sold through sale yards. This can be attributed to factors like the entry of restocker-focused saleyards into the National Livestock Reporting System (NLRS), a move away from traditional end-to-end production systems, an increase in direct consignment sales, and the growth of the feedlot sector.

The latter has played a crucial role in absorbing cattle not sold through sale yards, indicating a continued, albeit subtle, rebuild in the state.

Victoria’s cattle market dynamics have also shifted, particularly in relation to dairy cattle sales. Pre-2022, processor cattle sales exhibited regular seasonal peaks, but since then, there has been a noticeable decrease in dairy cattle transactions. This trend suggests a structural move away from dairy, potentially reshaping Victoria’s cattle industry landscape.

These developments across Australian states underscore the complexity of the cattle market, influenced by a mixture of seasonal cycles, industry shifts, and broader economic factors. As the industry moves forward, understanding these nuanced changes will be crucial for stakeholders to navigate the evolving landscape, ensuring strategies are aligned with current trends and future projections.